Let me begin with the GDP and its components:

First the GDP growth. As seen above we are lagging well below the median in GDP recovery. There have been worse Recessions but not many.

In contrast private investment is on the average and it means that companies are still investing in their infrastructure. This to a degree is bad news since it means further growth in productivity and lesser demand for labor. This we believe will be an increasing trend in our business cycle movements.

Despite the claims to the contrary the Government Expenditures are near bottom. This seems puzzling especially in light of the excess debt.

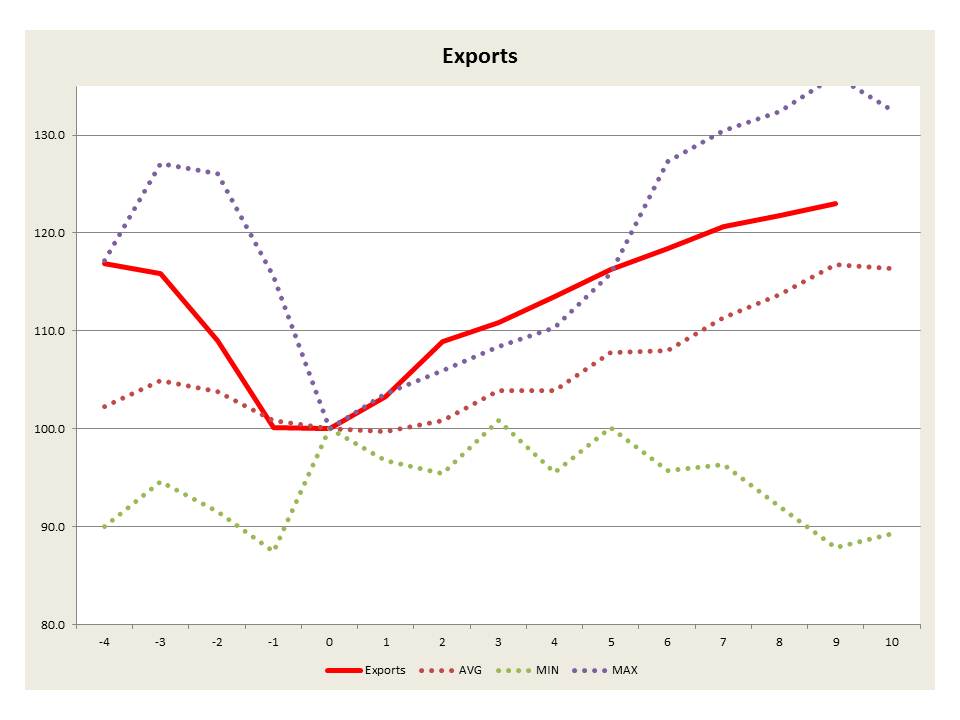

On the positive side we see strength in exports and in imports seen below.

Now as regards to Industrial Production we seem to be on average as seen below:

Yet the Income chart below is truly of concern. This is less of a 99% issue than the fact that income growth has staggered. Again our view if that this is driven by productivity changes.

Employment as above is as we expect at the bottom end. There is no sign of any recovery here and this should be a major concern of Government but in an election year and the current Administration we expect no changes.

Finally Retail Sales seems on average. One wonders where the source of income comes from to drive this. The upcoming Christmas Season will tell.